Market Commentary- Metals Team June 2022

![]()

By Mark Smith & Georges Lequime

After many weeks of heavy selling, we continue to see short term price volatility (3-6mth) for most of the commodity markets. Before Russia’s war began, the expectation was that the post-lockdown reflation trade would be undermined by the US Fed’s growth-slowing rate hike cycle/QT, and that global supply (mine, scrap) slowly recovers from lockdown.

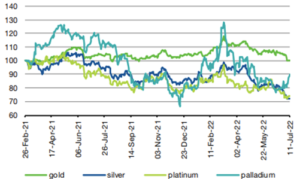

It's now mid-2022, and the US Fed’s not only determined to curb inflation via an aggressive combination of an accelerating rate hike cycle/QT, China’s covid-hit economic growth has stalled, and failing to respond to stimulus and Russia’s inflation-driving war continues. For the next 12 months, we remain positive on gold and silver which offers some capital protection, indeed gold has only lost 1% of its value since 12 months ago, demonstrating its role as a store of value.

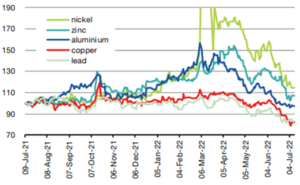

Figure 1 – Commodity price indices (12 mth rolling)

Base Metals Precious Metals

Source: Liberum

For the medium and longer term we are confident that we will continue to see elevated commodity prices. Commodity prices need to remain high enough for long enough to incentivise the allocation of capital to the sector. Capital allocation remains at 15 year lows despite the higher prices that we have witnessed through 2021 and this year (until very recently).

What has changed in recent weeks is that recession fears have come to the fore after the Fed’s hawkish stance on interest rates. Earlier this year, we reduced our exposure to the economically sensitive metals – copper and aluminium – to a bare minimum in anticipation of a global slowdown in economic activity. This paid off for us but we have really witnessed indiscriminate selling across all mining equities.

We expected lithium to continue to be a bright spot in the sector – which it has been – given the supply and demand imbalance that we see over the next two years. Yet lithium equities have sold off as well in recent weeks with market concerns about cost inflation. Again this brings us back to the circular argument that capital allocation to the sector is again slowing because of the lack of visibility on costs.

Where we have had to bear some pain in our investments is the gold and silver equities. We have maintained (and increased slightly) our exposure to gold and silver at around 55% of the portfolio as a risk diversifier, and given the value that we recognise in the listed gold and silver equities. Over the past few weeks, the gold price, and particularly, the silver price, have weakened with the selloff in stocks and bonds. A backdrop of rising interest rates, coupled with the expectation that the current high inflation figures are temporary, is putting investors off gold and silver as a safe haven trade for now with the US dollar very much in favour as the ultimate safe haven trade. Typically gold prices weaken into a recession and the start of the rate hike cycle, and then outperforms as the monetary policy responses to stimulate global economic activity are initiated. The timing and scale of the monetary policy responses are very difficult to predict. For this reason, and the fact that the gold and silver equities have become even cheaper in recent weeks, we continue to hold around 55% in gold and silver equities in the portfolio.

For the rest of the portfolio, we are positioned to own stocks exposed to commodities that the world is short of. Against global commodity price corrections, both nickel and lithium remain in positive territory (on 12 months) , up 15% and 434% respectively. During these volatile markets and low trading volumes, we are not touching the portfolio. We hold solid investments which are well capitalized, developing quality mining projects, which will once again regain investor interest after the summer doldrums.